If you're a small business owner, you may have heard of the acronym PCORI and the fees that come with it. But what is PCORI, and how does it apply to your organization?

Under the Affordable Care Act (ACA), sponsors of self-insured health plans must pay a fee to fund the federal Patient-Centered Outcomes Research Institute (PCORI). PCORI is an independent organization the ACA created to conduct research to help healthcare consumers make better decisions for their specific needs and outcomes. It also performs research related to clinical effectiveness.

Employers offering a self-insured medical reimbursement health plan, such as a health reimbursement arrangement (HRA), must pay this fee by July 31 each year via Form 7201. This fee was initially set to expire in 2019, but Congress extended it through September 30, 20292, due to the Further Consolidated Appropriations Act of 20203.

Takeaways from this blog post:

- Organizations offering self-insured plans, HRAs, and other specified health benefits must pay a PCORI fee annually via Form Yeah 720.

- The Secretary of Health and Human Services adjusts the fee rate annually for inflation. The fee for plans ending on or after October 1, 2023, and before October 1, 2024 is $3.22 per covered life.

- There are three methods for calculating the number of lives for PCORI fees on Form 720, including the actual count method, snapshot method, and Form 5500 Method.

Who owes the PCORI fee?

Specified health insurance policies subject to PCORI fees are generally prepaid health coverage arrangements with fixed premiums for accident or health coverage.

If your company offers a self-insured health plan, such as an HRA, you must pay the PCORI fee.

However, an integrated HRA isn’t subject to PCORI4 if an employer offers it alongside a self-insured plan from the same plan sponsor. In this case, the HRA and medical plan are considered a single plan for the PCORI fee.

An HRA that only covers dental and vision expenses is also exempt from the PCORI fee.

PCORI fees apply to organizations that offer different benefits, including:

- Specific fully insured plans

- Self-insured plans, including accident and major medical coverage

- HRAs

- Health flexible spending accounts (FSAs) if employer contributions exceed the greater of either the employee's contribution or $500

Which plans are exempt from the PCORI fee?

Some benefits, such as health savings accounts (HSAs) and other excepted benefits, aren't subject to the fees.

Health plans exempt from the PCORI fee include the following:

- Government programs, including Medicare, Medicaid, and the Children's Health Insurance Program (CHIP)

- Insurance policies that only provide excepted benefits, such as vision or dental

- Wellness programs (as long as the program doesn't provide significant medical care or treatment benefits)

- Policies that solely cover international employees

- Archer medical savings accounts (MSAs)

- Stop-loss or hospital indemnity

- Accident-only coverage

- Workers' compensation

How much is the PCORI fee?

For plans ending on or after October 1, 2023, and before October 1, 2024, the PCORI fee5 is $3.22 per covered life. That's up from $3 per covered life for plan years from a year earlier.

The Secretary of Health and Human Services adjusts the amount annually for inflation6.

|

Plan year |

PCORI fee |

|

On or after October 1, 2023, and before October 1, 2024 |

$3.22 |

|

On or after October 1, 2022, and before October 1, 20237 |

$3 |

|

On or after October 1, 2021, and before October 1, 2022 |

$2.79 |

What is IRS Form 720?

Organizations use Form 720, known as the Quarterly Federal Excise Tax Return8, to report any federal excise taxes collected.

This includes a variety of tax categories and fees, such as:

- Environmental taxes. This includes petroleum oil spill liability, products, and chemicals that cause ozone layer depletion. With these environmental taxes, you'll also have to complete IRS Form 66279.

- Communications and air transportation taxes. This includes phone service and air travel.

- Fuel taxes. This category includes fuel types such as diesel, kerosene, gasoline, and natural gas.

- Retail taxes. This is for trucks, trailers, and tractors.

- Ship passenger taxes.

- Foreign insurance taxes. This is for insurance that's issued by foreign insurers.

- Manufacturers taxes. This includes a long list of products and services, such as coal, tires, indoor tanning services, and vaccines.

- Other excise taxes.

- PCORI fees. These are for specified health insurance policies and applicable self-insured health plans.

Does your business need to submit IRS Form 720?

If you owe a PCORI fee, you must pay it using IRS Form 720 by July 31, following the last day of the plan year. If that date falls on a weekend or federal holiday, the PCORI fee is due on August 1. For self-insured health plans, see Part II, IRS No. 133 (b) of the form. If your business doesn't owe a PCORI fee, you don't need to complete IRS Form 720.

If you currently file Form 720, you will pay the fee with your second quarter return. If you don't regularly file Form 720, you only need to file the form once, during the second quarter, with your return. You don't need to file Form 720 on a quarterly basis.

What happens if you don't pay the PCORI fee?

David Blain is the CEO of BlueSky Wealth Advisors. Part of his role involves ensuring compliance with myriad financial and tax regulations that impact both his firm and its clients. Based on his experience helping clients with tax submissions, the importance of carefully managing the PCORI fee can't be understated.

"Forgetting or choosing not to pay this fee can lead to penalties and interest charges, which can be significant and add unnecessary costs," Blain said. "We've seen scenarios where entities miscalculated their covered lives or missed the fee payment deadline, and both situations led to complications during their annual audits and an increase in administrative burden to rectify the oversight."

If you don't report or pay10 the PCORI fee, you may face penalties similar to those for not filing a tax return. According to Internal Revenue Code §6651, the penalty is 5% of the excise tax due for each month or part of a month the return is late, with a cap of 25% of the unpaid tax.

"For employers and plan sponsors, I strongly recommend setting reminders for the reporting deadline, conducting a regular review of the number of insured members under applicable plans, and always maintaining open lines of communication with tax professionals," Blain said. "In instances where clients have forgotten to make their payments, acting swiftly to correct the oversight and promptly communicating with the IRS has helped in minimizing the penalties."

How to calculate the PCORI "number of lives"

According to Form 720 instructions, there are three ways to count the number of lives for plan years.

Here's what the instructions state for calculating the number of lives:

- The actual count method: Add the total of lives covered for each day of the plan year and divide that total by the total number of days in the plan year.

- The snapshot method: Take the total number of lives covered on one date (or more dates if an equal number of dates is used in each quarter) during the first, second, or third month of each quarter and divide that total by the number of dates on which you made a count.

- Form 5500 Method: Take the number of participants reported on Form 5500, Annual Return/Report of Employee Benefit Plan, or Form 5500-SF, Short Form Annual Return/Report of Small Employee Benefit Plan.

Additionally, there are special rules for calculating covered lives if you offer multiple self-funded plans or an integrated HRA from a medical insurance provider.

With an employer-sponsored HRA that's integrated with a fully-insured medical policy, it's only a requirement to pay the fee with respect to each HRA participant.

For multiple self-funded medical plans, you can treat them as a single plan for purposes of the fee. Each covered life is only counted once for the fee calculation.

You can view detailed information about “lives covered” in the final regulations11 document.

Does COBRA coverage to retirees or former employees count as "lives" covered?

Yes. You must count COBRA-covered individuals and dependents in the total number of lives for your benefit.

How to complete Form 720

New to filling out Form 720? We've compiled some examples. Below, the company plan covered an average of three participants and had a plan year that ended on December 31, 2021.

This section is included for informational purposes only. You should seek professional advice from a tax adviser or legal counsel to ensure proper compliance with the law.

Step 1: Complete company information header

The first part of this tax form asks for the basics, such as your name, address, and employer identification number, or EIN.

In the header, the quarter ending date will be June 30, 2022, as you're filing the form for the second quarter. Don't check “Final return” unless your organization is going out of business or you aren't required to file Form 720 in future quarters.

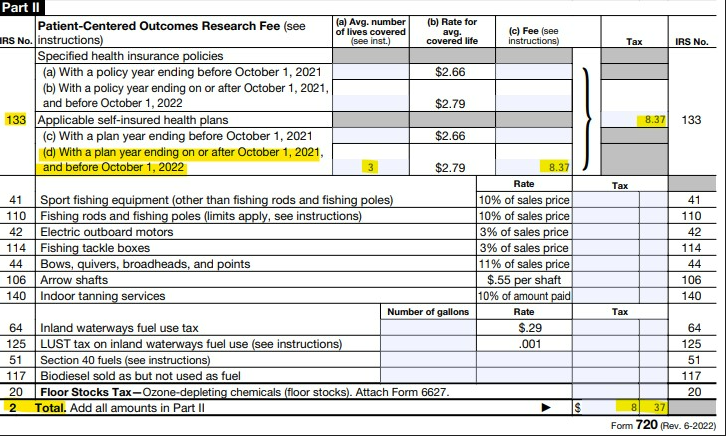

Step 2: Complete Part II, line 133(c) or (d)

Complete line 133(c) if your organization's plan year ended before October 1 of the previous year. In this example, the plan year ended in December, so we'd move on to the next section. Complete line 133(d) if the plan year ended on or after October 1 (this is the case with most plans). In this example, the plan did.

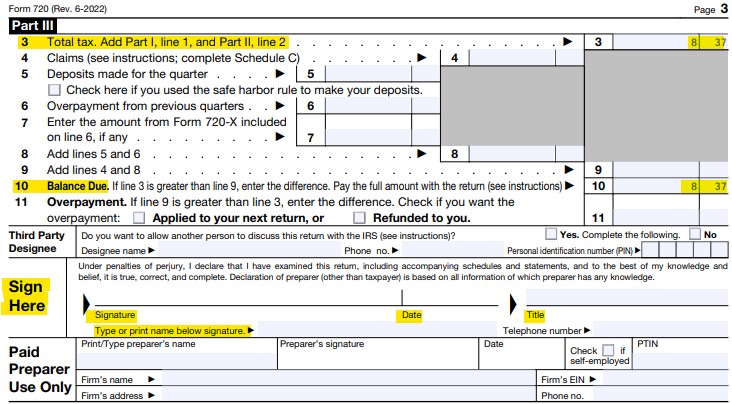

Step 3: Complete Part III lines 3 and 10, sign and date

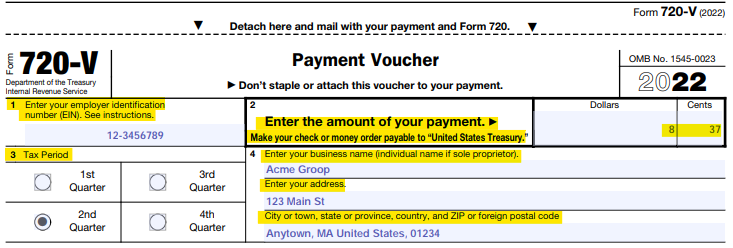

Step 4: Complete the payment voucher

Step 5: Send the completed form, payment voucher, and check to the IRS

You'll send Form 720 to the IRS in Ogden, Utah.

Send to:

Department of the Treasury

Internal Revenue Service

Ogden, UT 84201-0009

Conclusion

For applicable employers, the deadline for filing IRS Form 720 and paying PCORI fees is July 31. You should always reach out to a tax professional with your legal questions to ensure you're filling out your form and paying the fees correctly.

If you want a compliant, tax-advantaged health benefit for your employees, PeopleKeep can help! Our HRA administration software makes it easy to set up and manage your health benefit in minutes.

This blog article was originally published on August 4, 2020. It was last updated on May 23, 2024.

1. https://www.irs.gov/forms-pubs/about-form-720

2. https://www.irs.gov/newsroom/patient-centered-outcomes-research-institute-fee

3. https://www.congress.gov/bill/116th-congress/house-bill/1865

5. https://www.irs.gov/pub/irs-drop/n-23-70.pdf

7. https://www.irs.gov/pub/irs-drop/n-22-59.pdf

8. https://www.irs.gov/pub/irs-pdf/i720.pdf

9. https://www.irs.gov/pub/irs-pdf/f6627.pdf

11. https://www.govinfo.gov/content/pkg/FR-2012-12-06/pdf/2012-29325.pdf