Life has a way of complicating plans at work. Employees may get sick, injured, give birth, or need to care for a family member. In any of these situations, there are a couple of different ways your employee can take leave from work. Short-term disability and the Family Medical Leave Act (FMLA) are two options your employees can use. But sometimes, it’s hard to know the differences between FMLA vs. short-term disability.

This article will explain what FMLA and short-term disability are, who’s covered, and what qualifies for leave.

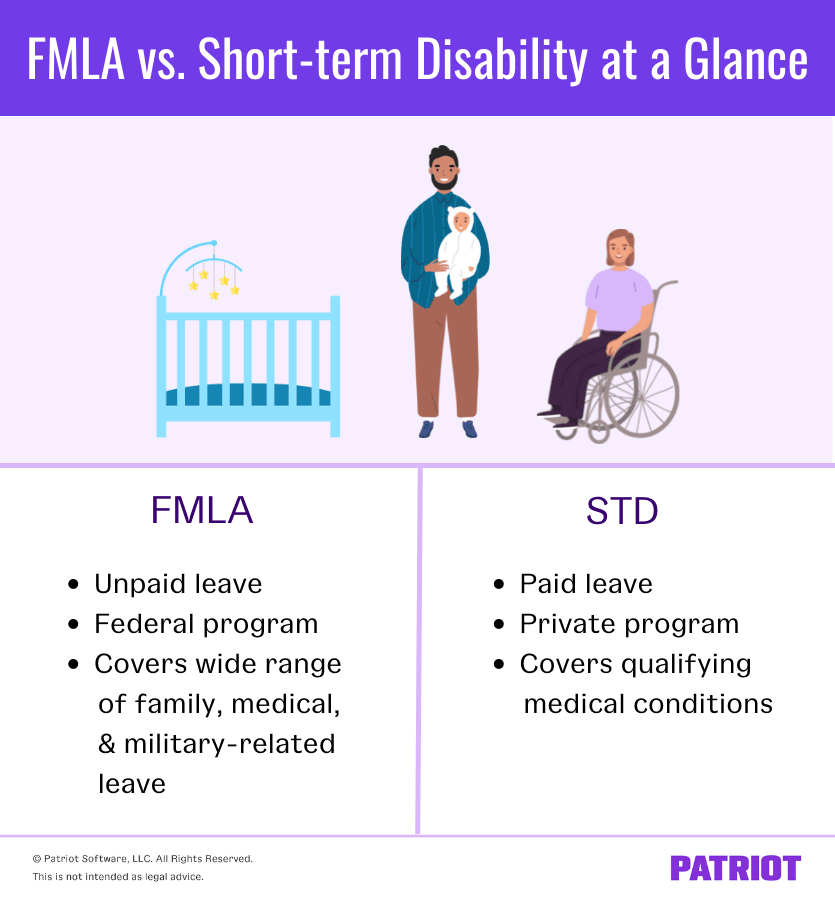

The difference between short-term disability and FMLA leave

Both short-term disability and FMLA provide leave to qualified employees who need time off from work. But, the two aren’t the same. So, what’s the difference between short-term disability and FMLA leave?

Short-term disability

Private insurance covers short-term disability (STD). To benefit from short-term disability, employees can opt in to an STD policy. You can offer short-term disability to your employees if you’d like. If not, they can purchase it themselves.

However, some states require employers to purchase short-term disability insurance for employees. There are currently five states with disability insurance requirements:

- California

- Hawaii

- New Jersey

- New York

- Rhode Island

Employers may be able to choose a state or private plan and decide how the policy is paid for (e.g., employer, employee, or both).

Percentage of wages covered

The amount of money an employee receives while on leave depends on the insurance policy. The money they receive can range anywhere from 60% – 75% of their gross wages. It works like this: The more they make + the more they (or you) pay for the policy = the more they receive while on leave.

Your employees shouldn’t be surprised if there’s a cap on how much money they get for the month. Leave wages are often capped between $5,000 and $6,500 per month.

Length of leave

Different insurance plans have different lengths of leave. More expensive policies generally offer the most extensive benefits. Leave can last up to 12 months. Such a variety can give you a wide range of control when it comes to choosing a short-term disability program for your employees. Just make sure you know what you are getting before you commit.

Who qualifies for short-term disability leave?

To qualify for short-term disability insurance, employees must meet the criteria set by the insurance provider.

The criteria for qualified employees vary from one insurance policy to the next. Some common factors include:

- An employee’s minimum earnings

- The length of employment

- Whether the employee can complete their job

Generally, only full-time employees are eligible, but there are exceptions to this rule. Pay close attention to short-term disability policies when deciding which one is right for your employees.

What qualifies for short-term disability leave?

What qualifies for STD is often specific to the insurance program. Generally speaking, any medical condition that renders the employee unable to work will qualify. Qualifying medical conditions often include:

- Pregnancy

- Illness

- Accidental injuries

- Major surgery

Paperwork

Only those employees who are already part of a short-term disability plan are eligible to access its benefits. Employees can’t apply to a plan retroactively or apply for a plan once they learn they need short-term disability leave.

If a covered employee needs to file a claim, they’ll need to:

- Contact you or HR for the proper forms

- Complete an application for STD leave

- Sign the proper documentation along with their doctor or physician

- Submit their application

- Be prepared to submit their medical records. Once they apply, you or the insurance company will review their medical records and make sure the records match the claim. Your employee may want to contact their doctor’s or physician’s office for the best way to share their medical records.

Pros and cons of short-term disability

Consider short-term disability pros and cons.

The pros of STD include:

- Qualified employees receive a percentage of their wages while on leave

- Leave can last up to 12 months

- A wide range of medical issues are covered

The cons of STD include:

- Certain conditions aren’t covered (e.g., preexisting conditions or time off to adopt a child)

- Job-related injuries aren’t covered

- Employee jobs aren’t guaranteed once leave is over

- Employees can be fired while on leave

- Health insurance coverage may not continue when employees are on leave

If an injury does happen at work, your employee should submit a workers’ compensation claim.

To avoid complications, make sure you and your employees are well versed in what is and isn’t covered in your short-term disability insurance plan.

FMLA leave

The Family and Medical Leave Act (FMLA) was created at the federal level to protect qualifying employees. FMLA allows qualified employees to take unpaid medical or family-related leave from work. This isn’t an insurance plan, so there’s nothing to purchase, and a large portion of employees are already covered simply because they work in the U.S.

Percentage of wages covered

FMLA offers employees unpaid leave for qualified family and medical reasons. It also protects the employee’s job while on leave.

However, it does not cover an employee’s wages since it is unpaid leave. So, FMLA covers 0% of an employee’s wages.

Length of leave

In most cases, eligible employees can take 12 weeks of FMLA-covered leave in a 12-month period. If the employee is caring for a family member who is also a service member with a serious illness or injury, they may be eligible for 26 workweeks of leave during a 12-month period.

Generally, FMLA leave is taken at one time. But there are specific circumstances that will allow employees to use intermittent leave.FMLA leave to be divided up over the year. Usually, this looks like a reduced schedule, either reducing hours in the work day or days worked in the week.

Who qualifies for FMLA leave?

Not all employees qualify for FMLA leave. To use FMLA leave, an employee must be personally eligible, and you must be an FMLA-covered employer.

To be an FMLA-covered employer, your company generally must be a:

- Private-sector employer who employs 50 or more employees within a 75-mile radius of its business

- Public agency (e.g., local, state, or federal government) regardless of the number of employees

- Public or private elementary or secondary school, regardless of the number of employees

Employees are eligible for FMLA leave if they:

- Work for a covered employer (and have for at least 12 months)

- Have more than 1,250 hours of service during the 12-month period preceding the leave

- Work in a location with at least 50 employees within 75 miles of the employer’s worksite

Remote employees are eligible as long as their main office has at least 50 employees within 75 miles of its location.

What qualifies for FMLA-covered leave?

FMLA-covered leave includes:

- The birth or adoption of a child

- Care for a spouse, child or parent with a serious health condition

- Health conditions that make it impossible for the employee to perform the essential functions of their job

- Any need arising from the military service of a spouse, child, or parent.

Paperwork

When possible, employees must request leave 30 days in advance. If the need for leave is a surprise, make the request as soon as possible. See the U.S. Department of Labor for all proper notices and applications.

Covered employers must:

- Provide notice to employees that explains their rights and responsibilities under the FMLA

- Include FMLA information in their employee handbook or upon hire

- Provide employees with notice concerning their FMLA leave eligibility when they request FMLA leave. You must also provide information concerning their rights and responsibilities as detailed by the FMLA

- Let employees know whether their requested leave qualifies as FMLA leave and if so the amount of leave that will be used.

Pros and cons of FMLA

FMLA has both pros and cons you’ll want to consider.

The pros of FMLA include:

- A wide range of medical, family, and military-related leave

- The program is free for qualifying employees

- Employee’s job is protected while on FMLA leave

The cons of FMLA include:

- The program doesn’t offer financial compensation

- The length of leave is usually only 12 weeks but under qualifying conditions be 26 weeks

FMLA vs short-term disability: Comparison chart

This is a lot of information to handle at once. Check out our chart comparing FMLA and short-term disability.

| Short-term Disability | FMLA | |

|---|---|---|

| Wages covered | 60%-75% of gross wages | No wages covered |

| Length of leave | Leave can last anywhere from a few weeks to 12 months | 12 weeks in a 12-month period |

| Who qualifies | Employees must meet the criteria set by the insurance provider. | Employees must work: – For a covered employer for at least 12 months – More than 1,250 hours during the 12-month period preceding the leave – In a location with at least 50 employees within 75 miles of the employer’s worksite |

| What qualifies | What qualifies for STD is specific to the insurance program. Generally speaking, any medical condition that renders the employee unable to work will qualify. Qualifying medical conditions often include: – Pregnancy – Illness – Accidental injuries – Major surgery | – The birth or adoption of a child – Care for a spouse, child or parent with a serious health condition – Health conditions that make it impossible for the employee to perform the essential functions of their job – Any need arising from the military service of a spouse, child, or parent. |

Looking for a better way to handle payroll for your small business? Sign up for Patriot Software today to get a free trial of the payroll software that’s top-ranked for functionality, ease of use, value for money, AND customer support.

This article has been updated from its original publication date of February 17, 2017.

This is not intended as legal advice; for more information, please click here.